It’s time for another spring property market update with the always brilliant Kellie Landrey – principal Buyer’s Agent at Scoutable – whose down to earth approach to property buying and accessible, relatable market insights always leave us feeling better informed.

Pure Finance: Kellie! Thanks so much for taking the time to do a spring property market check in with us again this year. It’s becoming a highly anticipated event…

Now we’re not sure about you, but it feels like we’ve had our busiest winter period yet and it looks like the spring buying season has actually kicked off early this year. Does that translate for you? What’s your ‘Buyers Agent’ take on the last few months?

Kellie Landrey: Hey team, it’s my pleasure! Thanks for chatting with me and I agree with you - It's been a busy winter from a ‘buyer activity’ point of view but from a ‘supply’ point of view, we are still light on.

According to CoreLogic, new listings (<30 days old) nationally have held above average since April this year, and for the four weeks leading to the 4th of August were sitting 1% higher than last year, and 7.7% above the previous five year average.

However, ‘despite the strong flow of new listings, the total national listings [aka, all listings] have been holding relatively steady, suggesting that the market is absorbing the above average flow of new listings’, right? So, over the four weeks leading up to the 4th of August, we are actually -1.7% below last year's levels, and -15.9% below the historical five year average.

So basically, even though stock levels are a little bit up from where they have been, they're not up enough to absorb buyer demand, which is leading to strong growth.

But whenever these statistics are given, they're usually given as national or capital city averages, right? And so inner city locations are always above or below the statistics. So, if the statistics are saying that stock levels are up but that's still not enough, then it's even worse in the inner city areas. And if they're saying that property prices have increased above average, then the inner city is going to be even more above that.

PF: Yeah and it feels like this can even happen on a suburb-specific level?

KL: Absolutely, and even on a property type level and at a price point level. So for example, in the Sydney market, what I'm finding right now is that inner city houses, especially at the $1.5M - $2.5M range, are light on stock so competition is still relatively strong. In the apartment market in the, say, $500k - early $1M range, the market isn’t quite as strong. Though there are, of course, always outliers.

What I'm also finding (and it's very similar to what I said to you last year) is that despite all the statistics, and despite everything that's happening in the market, what is still remaining true is: if a property is ticking all the boxes, it's flying. And if it has something a little bit ‘not quite right’ about it, it's struggling but still performing - it's not going backwards. For example, it might only have a couple of buyers on it, as opposed to an excessive amount of buyers on it. And that's especially true in the apartment market.

So yes, overall it has been busier, and everyone's feeling it.

PF: We’ve seen the Adelaide, Perth and Brisbane markets go from strength to strength, while recently released data has shown Melbourne prices starting to fall. There’s talk that we may even see Adelaide and Perth overtake Melbourne when it comes to median property value. What have you been noticing in these markets?

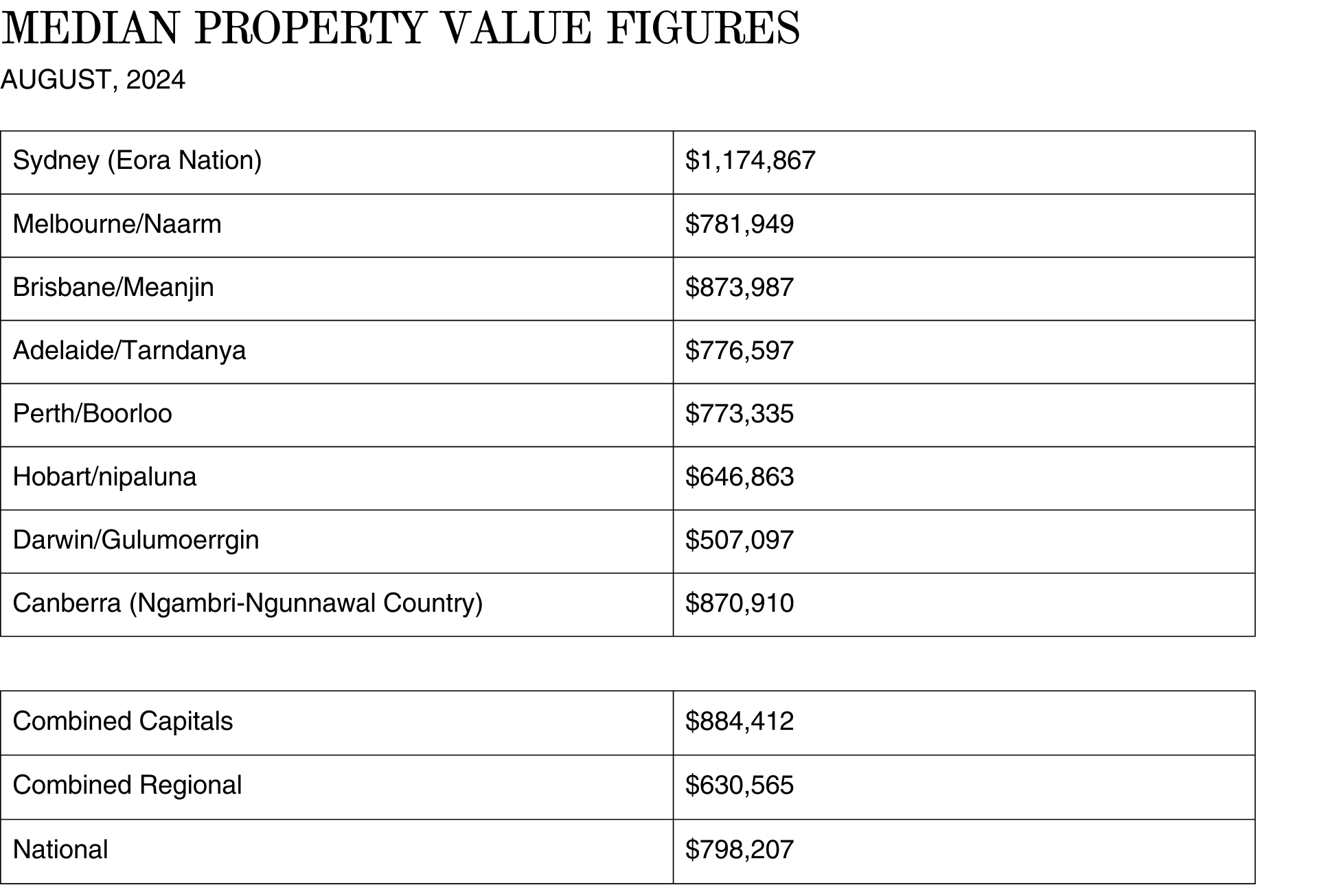

KL: Ok so, let’s take a look at some stats first, and then we’ll go into more detail. This is from the CoreLogic data released in early August, which shows:

- Sydney (Eora Nation) – is at 1.1% growth over the quarter and 5.6% growth over the year

- Melbourne/Naarm – is at -0.9% growth over the quarter and 0.2% growth over the year.

- Brisbane/Meanjin – is at 3.8% growth over the quarter and 16% over the year.

- Adelaide/Tarndanya – is at 5% growth over the quarter and 15.5% over the year.

- Perth/Boorloo – is at 6.2% growth over the quarter, and 24.7% over the year

- Hobart/nipaluna – is at -0.8% growth over the quarter and -1.2% over the year.

- Darwin/Gulumoerrgin – is at -0.3% growth over the quarter, and 2.3% over the year

- Canberra (Ngambri-Ngunnawal Country) – is at 0.5% growth over the quarter, and 1.7% over the year

SOURCE: Home Value Index, CoreLogic

Now, what the heck does it all mean? I think part of the reason Melbourne is struggling a little bit is because of their Covid Recovery Plan, with regards to the land tax situation, which has potentially seen a lot of investors retract from the market. I don't think it's necessarily the only reason why, but is perhaps one of the reasons people are finding it more attractive to invest in Brisbane or Adelaide over Melbourne.

I’ve spoken with a couple of local Melbourne experts and their thought process on the marketplace is that it's not going to turn around in a hurry. So, if people are considering investing in Melbourne, then they don't have to do it tomorrow, you know? They’re not going to miss the boat. But, what I would also say with Melbourne is don't impulse buy. Take your time and find the right property for you. Which is true for anywhere but you know, if you're worried about the Melbourne market running away from you, it doesn't seem like that's going to happen right now. Whereas somebody I spoke with in Brisbane said to me, you could potentially miss the boat and that, in 12 months time, it is going to accelerate even more. Though, whether or not that will be the case is another story…

But again, even though Melbourne is currently going through a flat period, it's not down so much that you would have wiped out your wealth. And as Jess Brady would say: you don't actually ‘realise the loss’ until you sell. So that's why it's also really important to find the right asset within the market you're looking at, because if you get a property that is very similar to 50 other properties in the suburb, but there may be that 5% that are more unique, then those ones are going to outperform the rest of the herd, which can help you in these kinds of fluctuating periods.

And Sydney, is just being Sydney.

PF: Yes exactly, it seems like Sydney just does not want to give up with the rising prices. You do a lot of work in the Sydney market - what have you been noticing?

KL: So, Sydney has recorded 1.1% growth over the quarter and 5.6% growth over the year, which shows the growth rates for Sydney are lower than Adelaide and Brisbane and, obviously, lower than Perth. But we all know that Perth can be risky for its connection to mining and so forth - you can make a lot of money in Perth, but you can also lose a lot of money in Perth. And if you look back at the ‘down times’ in the Perth cycle, you see that Perth can jump negative more quickly than other places.

But Sydney, whilst it's been low and steady growth in comparison to Brisbane and Adelaide, is still outperforming everywhere else on a 10 year average cycle.

And when I say Sydney here, I am really focusing on inner Sydney, as in, a 10km radius from the CBD, which is really where we're seeing things still performing really well. If you go to other areas of Sydney, or go further out, you might see more fluctuations in the market because of this supply issue. Or if you're in high rise in Green Square, Alexandria, for example, where there's 30 or 40 properties on the market on any given day, you might not see the same growth rates that, say, an apartment in Paddington or Newtown is getting. And again, it’s because there's less supply, so it does really all tie back to this supply issue.

So in summary, I'm seeing that the Sydney market is still continuing to perform well and that again, if the property is not ‘perfect’, then there could be a lower number of buyers on it. But generally speaking, it's going well, even though the stats are saying that growth rates are lower than other states.

I guess the very topical question for Sydney is: will it be possible for Sydney to keep rising at extreme rates when we have interest rates where they're currently at, coupled with the affordability constraints of people's incomes?

PF: Even though we’re a bit scared of the answer, what do you think?

KL: Well, access to a family guarantor/bank of mum and dad is a factor and then we've also got a large proportion of people in Sydney that are not first home buyers and who have already made a lot of equity from existing property and who are also fuelling the market.

PF: You also mentioned that you've been talking a lot with your clients about investment buying?

KL: Yes, I feel like I've got a reasonable amount of investors at the moment so, I think investors are coming back into the market.

PF: It sounds like Melbourne, Sydney and Brisbane is where most of your investor clients are kind of tossing up between. Is Brisbane where people are settling, based on what you were saying from the other experts based in those locations?

KL: Currently, Brisbane is where a lot of investors and rentvestors are considering and I’d say the main driving factor in people contemplating investing in Brisbane is because they want a house/land over an apartment. And, you know, I discuss with my clients at length about the fact that Brisbane can be really unpredictable, and you've really got to use an expert in Brisbane to make sure you're buying in an under supply location.

But especially for the people who have a sub million dollar budget for investing in Sydney, you know, that won't get you a house, that will get you an apartment. And it's just, considering the pros and cons of that.

But also, Melbourne isn’t necessarily a bad place to consider, as long as you can dive in and do your research and you’re able to absorb the land tax situation.

PF: And what about regional markets? Because, again, there's been some chatter about regional markets climbing back up because of affordability constraints?

KL: Yes so regional markets have been growing but are still lagging behind the capitals. There’s been a 1.3% gain across the combined regional areas for the last quarter, compared to 1.8% across the capital cities.

I feel like the regional market had its shining moment during covid. And so, I don't think they’re going to necessarily outperform capital cities, even within a flexible working environment. But also, and I say this to anyone considering regional for investment, you really don't want it to just be a lifestyle region. You want it to be an area that has multiple employment streams, or multiple reasons to make that area attractive.

Also, if people have two properties, they are likely selling their regional property before they're selling their main home, and so that market is always going to fall before capital cities, and that's the fluctuation in the regional markets. But if you can be in a regional market where it's not just tourism, or it's not just holiday homes and it's got other things going for it, then that will help lessen the burden of the risk.

PF: So, the August RBA meeting was another hold on the cash rate and while some were predicting one last rate rise, more recent data and information now suggests we are in waiting mode for our first rate cut. In your opinion, how has the RBA cash rate predictions affected the market so far in 2024, if at all?

KL: When I speak to some selling agents, they say, ‘oh, you know, I've got some vendors sitting on the fence and waiting to see what's happening with cash rates before they decide whether they're going to sell or not’. So the main impact that I'm seeing is tied to the supply level and of people ‘waiting and seeing’.

But in terms of the buying side, it's not really stopping people wanting to buy. This is because a lot of buyers out there will tell you that they think as soon as the rates drop, property prices are going to increase. And so, so they're not waiting for that to happen – they want to buy before the rates drop.

But in my personal experience, I'm not really noticing that it's an overly topical question amongst my clients.

PF: So, have you noticed an increase in properties being sold because the sellers' mortgage costs have become too expensive? Or not really?

KL: A little bit, but not so much that it would impact the statistics. But I've seen enough for me to notice properties that were bought mainly in that 2019 – 2021 range are selling again quickly. And the agents always like to say, ‘oh, you know, it’s a change in circumstances’, or they’ve ‘changed their plans’ or something along those lines. But I think that those people are probably the ones who bought during the time when interest rates were at the lowest, and are really starting to feel the pinch and are having to sell. But not enough that I could say to you that it's a definite trend.

PF: Hmmm that’s interesting. So, what sort of feedback are you getting from buyers and sellers at the moment, based on the properties that are or aren’t selling?

KL: Generally speaking, I’m seeing more people wanting to get a property that doesn't need work or is in a refurbished condition, because of the increased cost of construction. As an example, I had a client recently that was looking to renovate, and it was quoted as an $800k reno at the start of the pandemic. Then a few years later that same reno was going to cost $1.5M - almost double the cost. They ended up buying a property that was already renovated and a better property, in a very similar location, for less than the renovation cost. So I'm seeing a bit of that.

I'm also seeing a lot of people hesitant to buy apartments because of the defect issues happening across the board, but especially with properties built post 2000. There's a lot of water ingress issues that have been occurring in the last 5 to 10 years, and it's really starting to impact strata complexes that have not been managing their money well. There's also a lot of special levies and issues going on with apartments, so I'm seeing some people pull back on apartments for those reasons.

PF: Now we know that too much speculation can be a fool's errand but do you have any predictions for this spring buying season?

KL: Well firstly, I think the market is hard to explain as a whole but, having said that, there is always more activity in spring traditionally, and I don’t think that’s necessarily going to change this year. I think we are going to see more stock come on to the market, regardless of what interest rates do, because there is a bit of pent up supply with people that have been sitting on the fence. And people always need to buy and sell for various reasons, so more will come. If interest rates do drop, then we might see more of an influx of stock but I don't think it would be enough to go and make this huge impact – I think it's going to be absorbed.

The only thing that is going to truly change the market is if people find themselves under significant mortgage stress, [more than we’re currently seeing]. So if interest rates go up, and there's a large portion of people that really just can't afford it, then that might be an impactful change.

PF: Of course, nobody can ever *actually* predict what will happen with the property market and interest rates. But, we feel like things have become even more unpredictable post covid. What are your thoughts?

KL: Definitely. And look, this is a very general statement but, prior to covid times, if you’d been working in the industry for long enough and you did a lot of this kind of research, you could somewhat understand what the market movements were going to be moving forward, or where things were at in the cycle.

But since 2019/2020, things have become so much more unpredictable; in terms of how the market has performed in relation to the economy. We've had the lowest cash rate period in history, followed by the highest increase of interest rates in a short amount of time. Plus, we've got inflation pressures, all these things, right? We've also got every single media outlet telling us something different, month to month and then to add to the mix, we've now got a stock market that has basically shat itself.

And so, we're now in an environment where things are really unknown and it's all really confusing - for everyone! Because even the experts don't really know how the property market is going to react to the economy. And not only the Australian economy, but also the world economy.

I had a section in one of my newsletters at the beginning of the year where I summarised all the different economists' predictions for rate rises. And, they were all wrong. And I mean, these are the people that are meant to be the experts, right?

PF: Oh yeah, we had the exact same thing!

KL: And look, that’s not to say we should ignore it all, just more of an acknowledgement that nobody is ever entirely sure what interest rates are going to do.

Which is why we're not trying to ‘play the market’ here. You're trying to buy a home or a long term investment, and there's always going to be fluctuations in the market. Because regardless of what the last four or five years have done, if we look at the last 30 years, property values have always increased over the long term.

PF: And lastly, what are your tips for those braving the spring buying season this year?

KL: So it reverts back to the advice I gave last year, and the advice that I will probably continue to give, which is: you've got to internalise things a little bit in terms of: what is the plan for the property? What is your affordability? How is your employment sitting? Try and answer all those questions and then sort of run your own race.

I think it's also really important to go through your criteria of what you want the property to have, and give it some sort of weighted rating system. Are there things that I can't change about the property that I'm okay with and are there things I can change about the property that I can do in time? Does it meet all that sort of criteria? And that's the same for whether you're buying it for a home to live in or for an investment. And I would just go through this and focus on what's affordable for you, particularly if interest rates were to increase.

Also: research, research, research. Do your research on the location and whether it hits on those overriding principles of property investing in the sense of: is it an under supply location? Is there good infrastructure? You know, all those sorts of questions. Go and answer those questions, and then you can go and find your property with confidence.

Also, if you can, try and give yourself a cash buffer. That way, if there are any storms in the future - be it building defect issues that were unexpected, or otherwise - you have the ability to ride it out and not be forced to sell and ‘realise the loss’, as Jess says.

And as always, be prepared and pre-approved! This way, if you find a property you like, you can do all your due diligence quickly and go in confidently, either bidding at auction or by making a pre-auction offer.

If you're intending to make money out of property in the short term, then that's a very risky proposition, and it always is. No matter where we are in the cycle, it's very hard to beat the market, and it's even harder to do it now, when things are even more unpredictable.

PF: That is possibly one of the best paragraphs we’ve ever heard spoken about buying property, in terms of being honest, realistic and just ‘no spin’ kind of vibes. Sort of like ‘de-influencing’ but for the property market...

As always, thanks for the real talk, Kellie! These updates are always a breath of fresh air and we really appreciate you taking the time to share your insights with us and our community.

Keen for more?

→ See Kellie's top 10 tips for buying property in a hot market here.

→ Get insights from Kellie and Brendan on bidding successfully at auction here.

The information provided in this article is general advice only, and doesn’t constitute personal investment and/or financial advice. You should always reach out to us, or seek personal financial advice, before making any financial decisions.